There are several ways to protect your property from natural hazards. The proactive way is to strengthen your house to address specific hazards such as a flood. However, if there is still damage despite all your precautions, insurance can provide resources to aid recovery. Unfortunately, many homeowners do not find out until it is too late that their insurance policies do not cover flooding.

The National Flood Insurance Program (NFIP) offers a separate flood policy that protects for what most people is their single most important financial asset: their home. NFIP coverage is available to all owners of insurable property (a building and/or its contents) in a community participating in the NFIP. Renters may also obtain contents coverage through a NFIP policy.

An overview of the NFIP is on FEMA’s FloodSmart website. A list of participating Virginia communities can be found on the NFIP’s Community Status Book site. Not sure about the high costs associated with flooding? All it takes is a few inches of water to cause major damage to your home and its contents. FEMA’s NFIP website provides an interactive tool that demonstrates the cost of flooding and shows you what a flood in your home could cost, inch by inch. What are your chances of experiencing a flood? The site also includes animated flood risk scenarios that demonstrate how various factors impact different neighborhoods, providing excellent illustrations of where flooding can occur and the damage flooding does to a home. (Direct links to these tools can be found under the Useful Tools section of this website.)

All areas are susceptible to flooding to varying degrees, and flood insurance is an important consideration for all Virginia residents. Homes and businesses in high-risk flood areas having mortgages from federally regulated or insured lenders are required to have flood insurance. While flood insurance is not federally required, if you live in a moderate-to-low risk flood area, it is still available and strongly recommended: The NFIP reports that nearly 20 percent of flood insurance claims come from moderate-to-low risk areas.

No matter where you live, insurance professionals suggest that you prepare for severe weather disasters by creating a home inventory, which will create a record of what you own and what it is worth. A home inventory will help you estimate the value and replacement cost of your possessions in order to ensure that you have sufficient coverage under your homeowner’s or renter’s insurance policy. The inventory will create a detailed record of what you have in case disaster strikes and you need to provide your insurance company with a comprehensive list of what needs to be replaced. Visit knowyourstuff.org to create, save, and access a home inventory.

Natural disaster planning is one of the most important duties a homeowner can perform. Protection of life is first and foremost before, during, and immediately following a disaster. It is very important that consumers take time out before a disaster strikes to be certain that insurance concerns have been addressed. The following steps should be considered before homeowners are faced with a disaster:

- Contact your insurance company or agent and verify that coverage is in place before a disaster strikes. Make sure you have wind coverage protection and flood insurance if your home or business is located in a flood plain area.

- Make sure that you understand the deductible provision of your policy.

- Keep all of your insurance policies in an easily accessible location.

- If forced to evacuate, take copies of important paperwork, including your insurance policy and contact information for your insurance company or insurance agent.

- Be certain you understand the claim procedures of your insurance company.

- Make sure you have insurance up to at least 80 percent of the value on your home to avoid penalties under any co-insurance provision of your policy.

- Keep all necessary information regarding your health coverage, including prescription information, with your insurance records in the event of an evacuation.

- Be prepared to board up your windows and doorways to protect your home or business.

- Have a suitcase packed to last each member of your family for at least two to three days in case you need to evacuate from your home.

- In the event of a hurricane or flood watch, be sure that your vehicle has sufficient fuel in it in order to relocate to a safe area.

- Keep available a tarp and other supplies to protect your home in case it is damaged. An insurance policy usually requires the policyholder to protect the property from further damage.

Personal Property

Before a disaster occurs, take photographs or make a video of each room of your home and compile a set of records, old receipts, and bills to help establish the price and age of your property. Write down brand names and model numbers of appliances and electronic equipment and date purchased. Do not forget to list items such as clothing, sports equipment, tools, china, linens, holiday decorations, business equipment, hobby materials, and all other materials associated with your home or business.

Protect Your Home from Damage

Consumers can do a number of things to reduce the cost of their property insurance. Protecting property from possible damage before a disaster can have a major impact on insurers’ willingness to continue insuring the property and can also impact future prices the consumer will have to pay in the event their home is met by a disaster. By performing some of the following duties, consumers can make major contributions toward reducing the amount of losses occurring to their home:

- Consider adding storm shutters to the windows and doors of your home.

- Glue or nail down any loose shingles.

- Make certain yard items are tied down or secured. Bicycles, grills, toys, unsecured benches, and any other items not tied down should be placed inside an enclosed building. These items become missiles during a tornado or hurricane.

- If you own a vehicle, do not park it under a tree if a storm is anticipated.

- Take precaution to remove any tree that has the potential of damaging your home during a storm

Communicate with Your Insurance Agent

Check with your agent and policy declarations pages for information about what is covered:

- Coverage is typically provided in terms of replacement cost or the cost to rebuild your house.

- Does the policy have an inflation guard that increases each year as the cost to rebuild goes up? Construction costs have steadily increased and may increase even more so after a natural disaster.

- Additions or improvements to your house made since your initial policy purchase may not be covered, so it is important to have a periodic appraisal so that your coverage is adequate.

- Check with your insurance agent about possible discounts and incentives. Not all companies provide discounts for hurricane protective devices. These discounts over time can pay for the cost of certain retrofit upgrades.

- Understand your policy. Many policies cover only hurricanes and not lesser events such as a tropical storm or a tropical depression.

- Make sure you have coverage for (1) your main structure, (2) detached structures, (3) the contents in your house, and (4) expenses for loss of use (like hotel stays). Only the first item is required by mortgage lenders, so you may not have sufficient coverage for the remaining items.

The following are some things you need to think about when considering hurricane insurance:

- After a hurricane, there can be widespread damage and very few contractors or supplies available to perform repairs. This can result in an increase in cost to rebuild. Some homeowners have chosen to increase their insurance coverage by 30–40 percent to account for an expected spike in future construction costs after a hurricane.

- Additions or improvements to your house made since your initial policy purchase may not be covered, so it is important to have a periodic appraisal so that your coverage is adequate.

- Understand your policy. Many policies cover only hurricanes and not lesser events such as a tropical storm or a tropical depression.

- Basic insurance policies frequently just pay to restore a home structure to its before event condition. When building codes and ordinances change, you may be required to rebuild differently. Consequently, make sure that your policy includes law and ordinance coverage that will pay up to an additional 25% to 30% of the cost of rebuilding to cover any additional costs associated with meeting the latest building code requirements. If it isn’t automatically covered, it can usually be added for a relatively small additional premium.

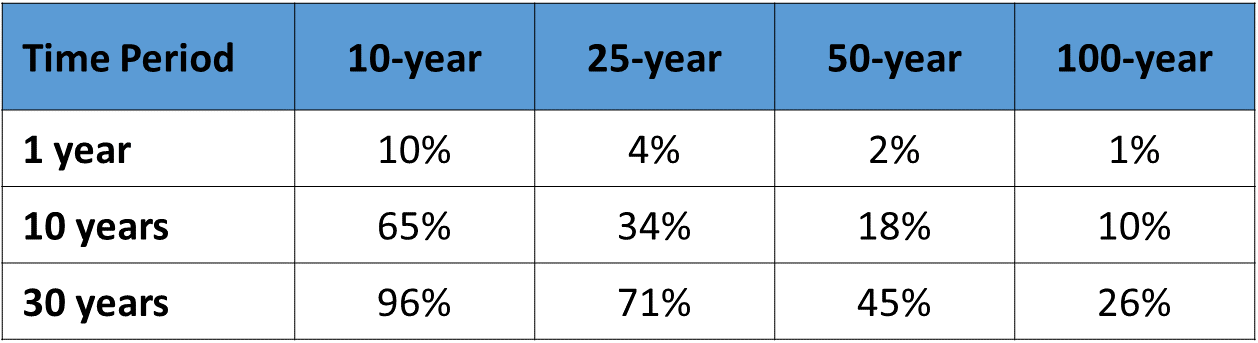

Floods are the most common—and most costly—natural disaster. In the past several years, about 60 percent of all declared disasters involved flooding. To obtain coverage from flood events, you need flood insurance. Standard homeowners’ insurance policies do not provide protection against floods. It is a hard lesson that has been learned by some in Virginia in the past, and it is an unfortunate reality that many people don’t find out until it’s too late. Just a few inches of water from a flood can cause tens of thousands of dollars in damage. According to FEMA, over the past five years the average paid flood insurance claim was nearly $34,000. Flood insurance is the best way to protect yourself from devastating financial loss. In areas with the greatest risk of flooding, Special Flood Hazard Areas (SFHAs), a building has a 26 percent chance of being flooded during a 30- year mortgage. On average, 25 to 30 percent of all flood insurance claims paid by the NFIP are for property outside of SFHAs. Homeowners, business owners, and renters can all buy flood insurance as long as their community participates in the NFIP.

While some private companies offer flood insurance, most flood insurance in the U.S. is backed by the federal government under the NFIP. Flood insurance is available to homeowners, renters, condo owners/renters, and commercial owners/renters in participating communities through local insurance agents. Costs vary depending on how much insurance is purchased, what it covers, and the property’s flood risk. NFIP rates are set and do not differ from company to company or agent to agent. These rates depend on several factors, including the date and type of construction of your home and your area’s level of risk. FEMA reports that the average flood insurance policy costs about $600 per year. Residential property owners located in low-to-moderate risk areas should ask their insurance agents if they are eligible for the Preferred Risk Policy, which provides very inexpensive flood insurance protection. If your community participates in the Community Rating System (CRS), you may qualify for an insurance premium discount—in some communities of up to 45 percent—if you live in a high-risk area and up to 10 percent in moderate-to-low risk areas.

You should discuss insuring personal property with your agent, since contents coverage is optional. Typically, there’s a 30-day waiting period from date of purchase before your policy goes into effect. That means now is the best time to buy flood insurance—don’t wait until a storm is approaching. Visit the Learn More section of this website to find links to the NFIP and FEMA websites to get more information about finding flood insurance for your area.

- Chart reproduced from Recurrent Flooding Study for Tidewater Virginia, Virginia Institute of Marine Science, accessed at http://ccrm.vims.edu/recurrent_flooding/Recurrent_Flooding_Study_web.pdf, July 2016.